If you’ve ever glanced at your KiwiSaver balance and wondered how you’re tracking against other Kiwis, you’re not alone. While personal circumstances vary, there are benchmarks based on national data that can help you gauge where you stand—and decide whether it’s time to step things up. Here’s what recent figures reveal, what they mean for your financial future, and how to bridge any gaps.

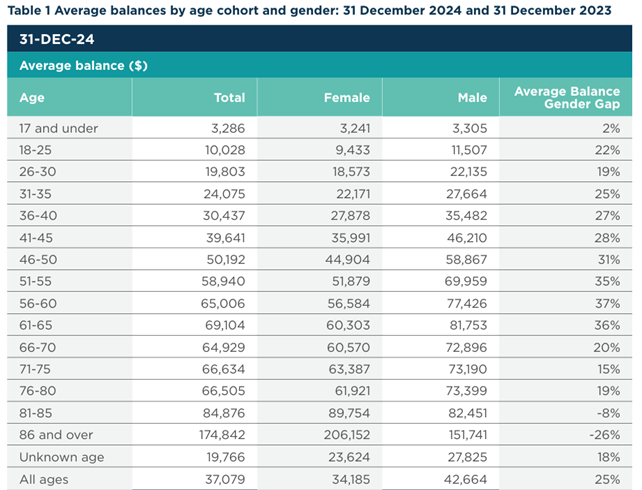

According to the latest data from the Retirement Commission (commissioned from actuaries Melville Jessup Weaver), as of 31 December 2024, the average KiwiSaver balance across all New Zealanders was $37,079, a 16.5% increase from the prior year. Men held an average of $42,664, while women trailed at $34,185, reflecting a persistent 25% gender gap.

When broken down by age, the average balances were:

At face value, these numbers might feel a bit light. After all, studies suggest a single homeowner aiming for a comfortable retirement today may need $270,000, while couples could require anywhere from $450,000 (rural) to $1.1 million (city).

But averages don’t tell the full story. They’re skewed by outliers and don’t account for individual factors like home-ownership, other savings, or when you started contributing. Still, these benchmarks are a useful reality check, especially when paired with projection tools like those offered by Sorted.co.nz and KiwiSaver providers, which can help you estimate your likely retirement income based on your current trajectory.

By age 30

Aim to have around $20,000 in your KiwiSaver. If you’re hitting that, you’re not falling behind the national average and… you’ve started planning for your retirement early, which means you are building good savings habits and are starting young so that compound returns are working in your favour.

At this age and stage, you may have used – or be thinking about using – your KiwiSaver to help purchase your first home. So it’s important to make sure that your fund matches your risk profile and goals.

By age 40

If you’ve hit your forties and your balance is within the $30,000–$45,000 range, the Retirement Commission benchmarks show you’re tracking with peers. At this stage, it’s smart to reassess your contribution rates and fund choice. Are you invested in a growth fund? Could increasing contributions bring you closer to long‑term comfort levels?

By age 50

At this stage it’s likely that retirement is no longer feeling like a distant concept. Sorted.co.nz suggests that by 50, you should be thinking in terms of whether your balance is on track to provide the lifestyle you want, not just whether you’re hitting averages. Aiming for at least three to four times your annual salary in KiwiSaver and other investments by this point is a reasonable guide. For example, if your household earns $150,000, a combined balance of $450,000–$600,000 across KiwiSaver and other retirement savings helps ensure you’re well positioned to build further in your final peak earning years.

By age 60

With only five years until you can gain access to your KiwiSaver at 65, your fund should now look much closer to its end goal. Benchmarks suggest targeting seven to eight times your annual salary by this stage, supplemented by other savings or investments. For a household earning $200,000, that means aiming for $1.4-$1.6 million in combined retirement savings.

While that number may feel daunting, remember that KiwiSaver balances can accelerate quickly in your later years due to compounding, higher contributions and investment growth. This is also the time to chat with your adviser to review your fund type and consider whether a more balanced approach is appropriate as you near the point of drawing down your savings.

The 25% average difference between men’s and women’s KiwiSaver balances isn’t a fluke. According to the Retirement Commission, it stems from systemic issues like care-related / maternity breaks, part-time work, and long-standing pay disparities. Being aware of these issues and adjusting your savings rate to take this into account can make a substantial difference over time.

If your current balance trails the average, don’t panic, it just means you have room to grow. Here are some steps to consider:

Knowing how much KiwiSaver others your age have won’t tell the whole story, but it’s still a relevant benchmark. At 30, being near (or above) $20,000 – $30,000 gives you a solid footing. In your 40’s, $40,000-$50,000 signals you’re on track, but it’s also a critical time to fine-turn your contributions and strategy. By 50, you should be aiming for three to four times your annual salary in combined savings, and by 60, seven to eight times. However, it’s less about hitting one ‘right’ number and more about being intentional and informed.

Regardless of your age, reviewing your KiwiSaver fund every few years to ensure it is aligned with your retirement goals is highly recommended.

If you think a KiwiSaver review might help you get on track, book a free chat today with one of our specialist advisers. They can help you assess whether you are on track to hit your retirement goals and also whether you are in the right fund for your age, stage and risk profile. Plus, book a free review this month and go in the draw to win a month’s free mortgage repayments on us!

To book your review, click here.

Not quite ready to book a chat? You can also use our free online questionnaire to find out your investor type and what KiwiSaver fund type is right for you. Click here to fill in this quick questionnaire and to find out your results.

The content of this article should not be taken as financial advice, or a recommendation of any financial product. These insights are based on current economic commentary, market pricing for interest rates, and our personal opinion. Threefold is not liable or responsible for any information, omissions, or errors present.